Juggling tuition fees, hostel rent, and rising food costs hits Nigerian students hard. Inflation pushes prices up by double digits each year, making every naira count. A solid savings account isn’t a luxury—it’s a tool to build stability amid these pressures. Unlike current accounts that offer no growth, savings options earn interest and encourage habits that pay off long-term. This guide breaks down the best choices to help you pick one that fits your life on campus.

Table of Contents

Introduction: Navigating Student Finances in the Nigerian Landscape

Tuition deadlines loom, and pocket money from home stretches thin. Many students in Nigeria face upkeep costs that eat into allowances quickly. A dedicated savings account changes that by letting your money work for you. It beats stuffing cash under the mattress or relying on zero-interest current accounts. Banks now offer plans built for your needs, from easy access to higher returns. You can start small and watch it grow, easing worries about unexpected bills like textbooks or medical fees.

Understanding Student Banking Needs in Nigeria

Students in Nigeria deal with tight budgets and irregular income from part-time gigs or family support. You need accounts that match this reality, not ones designed for full-time workers. Focus on options that keep things simple and cost-free where possible.

Key Features to Prioritize in a Student Account

Look for accounts with no opening balance or just N100 to start. Digital access matters too—USSD codes let you check balances without data, perfect for spotty campus Wi-Fi. Security comes first; pick banks with two-factor authentication and fraud alerts. Apps from banks like GTBank or OPay make transfers fast, so you can send money home or pay bills without leaving class.

Common Pitfalls: Hidden Fees and Charges to Avoid

Maintenance fees can wipe out small savings if your balance dips below N5,000. Watch for inter-bank ATM charges through NIBSS, which add up to N35 per withdrawal outside your bank’s network. Always check the terms for dormancy fees after six months of no activity. Read the fine print on the bank’s site or app before signing up. Ask a branch rep about any promo rates that expire after three months.

The Role of Regulatory Bodies (CBN Guidelines)

The Central Bank of Nigeria sets rules to protect you. They cap savings interest at market rates but ensure fair charges under the Guide to Bank Charges. Deposits up to N500,000 get NDIC coverage if things go wrong. This setup gives peace of mind when choosing any licensed bank. Follow CBN updates on their site to stay informed about new rules, like BVN requirements for all accounts.

Top Traditional Banks Offering Student Savings Packages

Big banks have branches everywhere, from Lagos to university towns like Nsukka. They suit students who value face-to-face help and widespread ATMs. Rates stay modest, but reliability counts when you need quick cash.

Analysis of Tier-1 Bank Student Offerings (e.g., Access, Zenith, GTBank)

Access Bank’s Solo Account targets undergrads with easy setup and campus events. Zenith’s Aspire Account lets 16- to 25-year-olds open with zero balance and caps at N10 million for safety. GTBank’s GTCrea8 e-Savers works for ages 16 to 25, with strong ATM access near schools. These plans often include free debit cards for daily use. Pick based on your school’s location—GTBank shines in the south, Zenith in the north.

Interest Rate Benchmarks and Account Maintenance Structures

Access Solo pays 8.25% per year, higher than most peers. Zenith Aspire offers 5.5% annually, with no monthly fees if you keep it active. GTBank GTCrea8 gives 5.25%, and they waive charges for balances over N1,000. Traditional banks charge tiers: under N5,000 might cost N100 monthly, but student plans often skip that. Compare on sites like nairaCompare for the latest figures.

Digital Onboarding Experience for New University Entrants

Opening an account takes minutes via apps. Access lets you upload your student ID and BVN online, no branch visit needed. Zenith’s Aspire uses their mobile site for quick setup, even from your hostel. GTBank requires a selfie and matric number for GTCrea8. All follow CBN’s BVN rules, so link it first. New students away from home appreciate this—no paperwork queues during freshers’ week.

Exploring Fintech and Digital-First Savings Alternatives

Fintech apps disrupt old banking with better rates and no queues. They appeal to tech-savvy students who handle everything on phones. Growth comes faster here, but check app stability first.

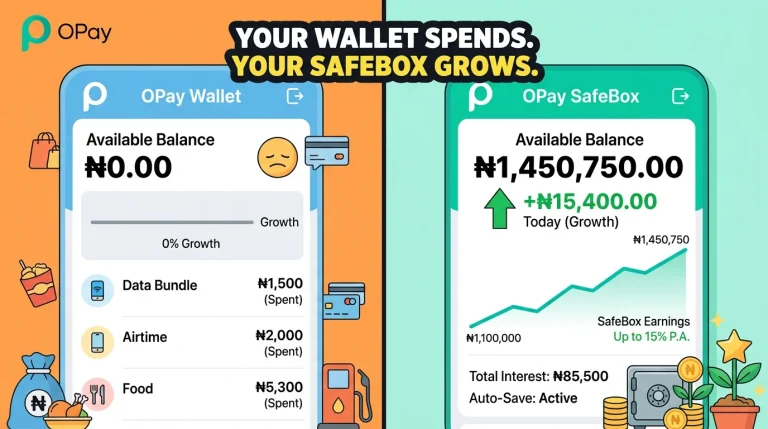

High-Yield Savings Options with Zero Monthly Fees

OPay’s OWealth pays 15% on the first N100,000 and 5% after, with no fees. Moniepoint offers up to 16% on savings starting at N1,000. Kuda keeps it free with basic interest around 10%, plus cashback on spends. These beat traditional rates by double in some cases. Download from Google Play and start saving in under five minutes.

Goal-Oriented Savings Tools and Automated Transfers

Set up “pockets” in OPay to lock money for tuition. Moniepoint’s app auto-transfers 10% of income to savings. Kuda rounds up purchases and saves the change. Use these for goals like laptop funds or travel home. Track progress with charts in the app—it keeps you motivated.

Security and Deposit Insurance in Digital Banking

NDIC covers fintech deposits up to N500,000, same as banks. OPay and Moniepoint use biometric logins and real-time alerts. Kuda blocks suspicious logins instantly. Stick to CBN-licensed apps to avoid scams. User reviews on Trustpilot praise their uptime during peak times.

Specialized Savings Products: Beyond the Basic Account

Some accounts add extras for global needs or growth. They help if family sends dollars or you eye investments. Start basic, then upgrade as you learn.

Savings Accounts Linked to International Transactions (Forex Access)

GTBank’s account ties to a dollar wallet for easy conversions. Access Bank’s forex option handles remittances without high fees. OPay supports USD transfers at market rates. This saves on exchange losses if parents abroad wire money. Rates hover at 1% commission—better than black market deals.

Micro-Investment Linkages for Advanced Students

Zenith links Aspire to money market funds yielding 10-12%. Moniepoint offers treasury bills via app, starting at N5,000. GTBank’s tools let you invest spare cash in low-risk bonds. Returns beat savings alone, but read risks first. It’s a step up for final-year students planning post-grad life.

Utilizing Fixed Deposit Options for Emergency Funds

Lock N10,000 in Moniepoint’s fixed deposit for 18% over six months. Access offers 7-9% on year-long terms. Use for emergencies like health costs—break early with minor penalties. Keep some liquid for daily needs, but fixed grows the rest. Check tenures on bank sites to match your timeline.

Actionable Steps to Maximize Student Savings Growth

Reviews are done—now put it to work. Build habits that turn small deposits into real security. Start today for compound effects.

Creating a Realistic Student Budget That Supports Saving

Adapt the 50/30/20 rule: 50% for essentials like food, 30% for fun, 20% to savings. Track via GTBank’s app or a notebook. Cut data bundles by using free campus Wi-Fi. Apps like OPay show spending patterns weekly. Aim to save N2,000 monthly—it adds up.

Leveraging Student Discounts and Loyalty Programs

GTBank gives data top-ups for active GTCrea8 users. Zenith offers book vouchers through Aspire partnerships. OPay runs student promos for free transfers. Sign up for these to stretch your naira. Check bank social media for campus deals.

Automated Savings: Setting It and Forgetting It

Link your allowance account to auto-save N500 weekly in Kuda. OPay deducts after salary alerts. This builds without thinking. Review quarterly to adjust. Consistency turns N10,000 into N12,000 yearly at 8% interest.

Conclusion: Securing Your Financial Foundation in Nigeria

The best savings accounts for students in Nigeria mix ease, growth, and trust. Traditional picks like Access Solo or GTBank GTCrea8 provide solid access, while fintechs such as OPay and Moniepoint deliver higher yields up to 16%. Balance digital speed with bank reliability to avoid risks. Your choice shapes academic focus and future plans. Open an account now—download the app, verify your BVN, and deposit your first N1,000. Start building that foundation today.